(Bloomberg) — US consumer borrowing increased in March by more than expected on one of the largest spikes in credit-card balances on record.

Total credit increased $26.5 billion, the most in four months, after a February gain of $15 billion, Federal Reserve data showed Friday. The figure, which isn’t adjusted for inflation, compared with the median estimate of a $17 billion increase in a Bloomberg survey of economists.

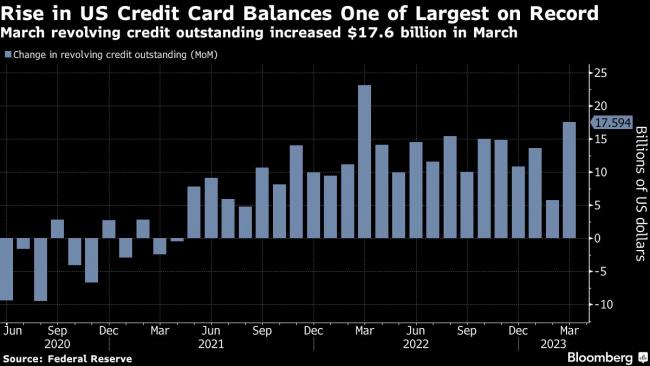

Revolving credit outstanding, which includes credit cards, jumped $17.6 billion, about three times the prior month’s gain and the largest in a year.

While low unemployment continues to be a key support for consumer spending, many Americans are beginning to pull back and save more. Others, however, are struggling to make ends meet — with some leaning on credit cards to do so.

A recent poll by Morning Consult for Bloomberg News showed over half of Americans don’t have the financial resources to cover a surprise $400 expense without taking on debt.

The Fed’s report showed non-revolving credit, such as loans for school tuition and vehicle purchases, rose $8.9 billion. The increase suggest that, at least at the consumer level, borrowing for big purchases is holding up in the face of tighter credit conditions.

The banking turmoil that has rattled markets and reinforced many economists’ expectations of a recession later this year started in March with the failure of Silicon Valley Bank. Since then, two other American banks have failed, and concerns are mounting about the economic impact from tighter credit conditions.

Source: Investing.com

{kind=link}